Your Credit Score and FHA Loans

Your credit score plays a big role in determining how your mortgage experience turns out. A good one can help you secure a low interest rate mortgage with a smaller down payment, because it shows lenders that you’re creditworthy. On the other hand, a lower score can severely hurt your chances of getting approved for a loan.

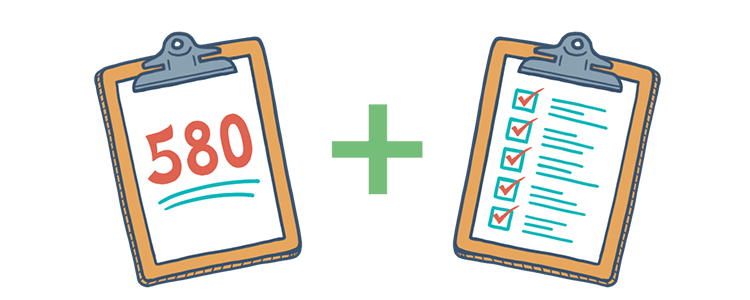

What makes a good score? What score do you need for lenders to consider you a “good risk”? We’ve compiled some important information about credit scores and reporting that will help you understand exactly what that number represents in an effort to help you increase it to where your lender needs it to be.

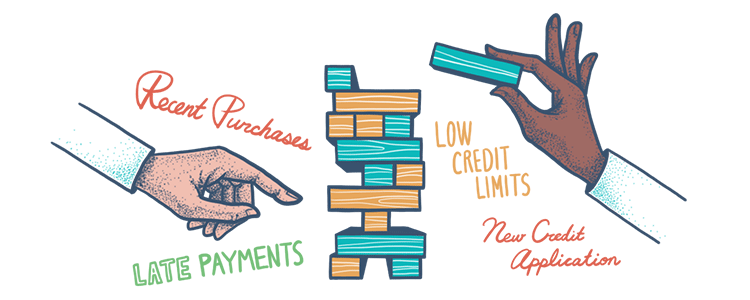

Borrowers hear the term “credit report” a lot when they enter the homebuying market, but don’t always know what goes into it. Your credit report is compiled with different information about your spending and payment habits. Learn about all the factors that go into your credit score, what a FICO score really means, and what credit bureaus really do.

Even if you’ve made some mistakes in the past, it is possible to improve your credit score if you decide to put in the work. But before you can fix the problem, you need to know the point you’re starting at. Read about the steps you can take to increase your score so you can ensure a low-interest loan when the time comes for you to apply for a mortgage.

When shopping for a mortgage, many people will tell you what is and isn’t good for your credit score. They might give you advice about the dos and don’ts to help you keep your scores up. But it’s likely that you’ve come across some misinformation along the way. Read the facts about what affects your score, and check out some of the credit score myths as well!

While the Federal Housing Administration has set low credit score requirements for the loans they will insure, lenders providing the mortgages may not approve a loan for borrowers with lower scores. It is very common that lenders have their own, additional requirements for FHA loans that they grant, generally called “overlays.”

FHA Loan Articles

February 12, 2024When you are approved for an FHA One-Time Close Construction loan, you get a single loan that pays for both the costs to build the house, and serves as the mortgage. One application, one approval process, and one closing date.

November 22, 2023In the last days of November 2023, mortgage loan rates flirted with the 8% range but have since backed away, showing small but continued improvement. What does this mean for house hunters considering their options to become homeowners soon?

November 4, 2023In May 2023, USA Today published some facts and figures about the state of the housing market in America. If you are weighing your options for an FHA mortgage and trying to decide if it’s cheaper to buy or rent, your zip code may have a lot to do with the answers you get.

October 14, 2023FHA loan limits serve as a crucial mechanism to balance financial sustainability, regional variations in housing costs, and the agency's mission to promote homeownership, particularly for those with limited financial resources.

September 25, 2023Mortgage rates are hitting prospective homeowners hard this year and are approaching 8%, a rate that didn't seem very likely last winter. With so many people priced out of the market by the combination of high rates and a dwindling supply of homes.

September 19, 2023The FHA Handbook serves as a crucial resource for mortgage lenders, appraisers, underwriters, and other professionals involved in the origination and servicing of FHA-insured home loans. It outlines the policies and requirements for FHA-insured mortgages.