Understanding FHA Loan Debt Ratios

July 29, 2023

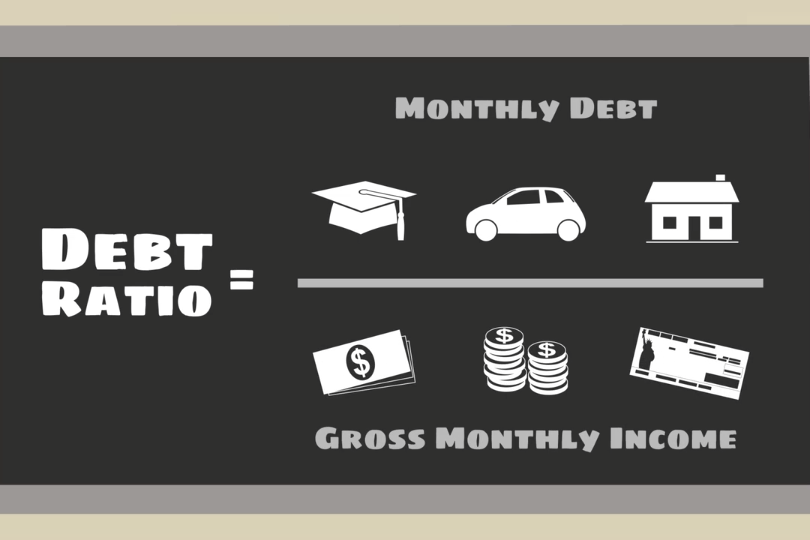

FHA loan debt ratios are financial benchmarks that assess a borrower's ability to manage their debt and make mortgage payments on time. These ratios play a pivotal role in the FHA loan approval process, as they provide a snapshot of a borrower's financial health. Two primary debt ratios are considered when evaluating an applicant's eligibility for an FHA loan:

Front-End Ratio (Housing Ratio)

This measures the percentage of a borrower's monthly gross income that will be allocated to housing-related expenses. These expenses include mortgage principal and interest, property taxes, homeowners insurance, and mortgage insurance premiums (if applicable). FHA guidelines typically require that the housing ratio does not exceed 31% of the borrower's gross income.

Back-End Ratio (Total Debt Ratio)

This is a broader measure of a borrower's debt load. It considers not only housing-related expenses but also other monthly obligations such as car loans, credit card payments, student loans, and any other outstanding debts. The FHA generally sets a maximum allowable back-end ratio of 43% of the borrower's gross income.

To improve your back-end ratio, focus on paying down existing debts, such as credit cards and personal loans. Reducing your overall debt load can make you a more attractive candidate for an FHA loan.

Both of these ratios serve as vital tools for lenders to assess your financial health and determine your eligibility for financing. By managing your debt wisely, increasing your income, and budgeting carefully, you can improve your debt ratios and increase your chances of securing an FHA loan. Remember that while debt ratios are an essential part of the approval process, they are just one piece of the puzzle, and other factors like credit score and down payment also play a role in determining your loan eligibility.

------------------------------

RELATED VIDEOS:

Let's Talk About Home Equity

Understanding Your Loan Term

Your Home Loan is Called a Mortgage

FHA Loan Articles

January 10, 2023When getting ready to shop for a home loan, it's worth taking a look at your credit report. Your credit score is a big factor when lenders take a look at your loan application, and it plays a huge role in the interest rate you get.

December 23, 2022When it comes to buying a house, saving up for a down payment can be one of the most overwhelming aspects. While down payments are one of the biggest obstacles for many in the mortgage process, it helps to understand the ins and outs of why they play such a big role.

November 30, 2022Buying and financing a home is complicated and can become overwhelming. It's important for you to stay informed, and know what your options are. So, start with the basics and read about the four different mortgage types available before approaching a lender.

November 8, 2022The fact is that repairs and renovations to your home cost a lot of money. Luckily, the FHA has an option for those with fixer-uppers on their hands. The FHA 203(k) Rehabilitation Mortgages allows borrowers to finance the funds for renovations to a home.

October 17, 2022If you’ve begun your search for a new home and are looking into mortgage options, you’ve likely heard of mobile, manufactured, and modular homes. While people working in real estate throw these terms around easily, it might be something that leaves everyday homebuyers confused.