Understanding FHA Loan Debt Ratios

July 29, 2023

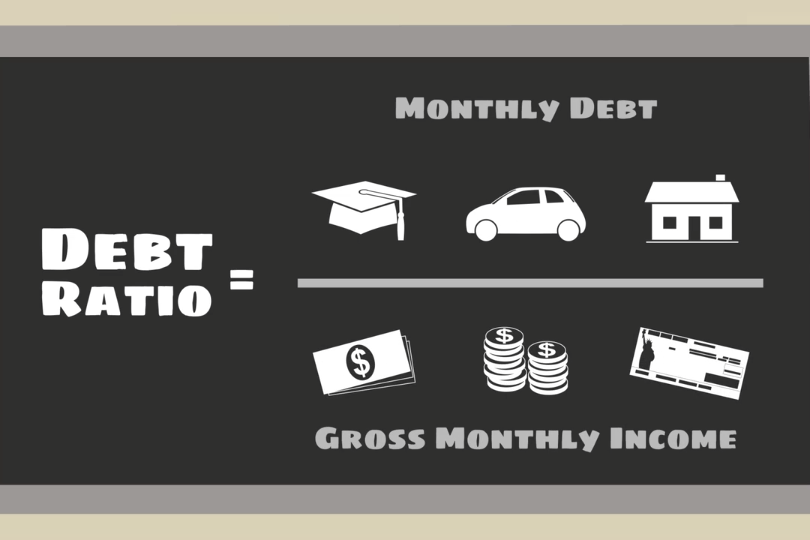

FHA loan debt ratios are financial benchmarks that assess a borrower's ability to manage their debt and make mortgage payments on time. These ratios play a pivotal role in the FHA loan approval process, as they provide a snapshot of a borrower's financial health. Two primary debt ratios are considered when evaluating an applicant's eligibility for an FHA loan:

Front-End Ratio (Housing Ratio)

This measures the percentage of a borrower's monthly gross income that will be allocated to housing-related expenses. These expenses include mortgage principal and interest, property taxes, homeowners insurance, and mortgage insurance premiums (if applicable). FHA guidelines typically require that the housing ratio does not exceed 31% of the borrower's gross income.

Back-End Ratio (Total Debt Ratio)

This is a broader measure of a borrower's debt load. It considers not only housing-related expenses but also other monthly obligations such as car loans, credit card payments, student loans, and any other outstanding debts. The FHA generally sets a maximum allowable back-end ratio of 43% of the borrower's gross income.

To improve your back-end ratio, focus on paying down existing debts, such as credit cards and personal loans. Reducing your overall debt load can make you a more attractive candidate for an FHA loan.

Both of these ratios serve as vital tools for lenders to assess your financial health and determine your eligibility for financing. By managing your debt wisely, increasing your income, and budgeting carefully, you can improve your debt ratios and increase your chances of securing an FHA loan. Remember that while debt ratios are an essential part of the approval process, they are just one piece of the puzzle, and other factors like credit score and down payment also play a role in determining your loan eligibility.

------------------------------

RELATED VIDEOS:

Let's Talk About Home Equity

Understanding Your Loan Term

Your Home Loan is Called a Mortgage

FHA Loan Articles

April 18, 2023Your lender is required to make sure you can realistically afford your mortgage, and that means verifying that your income is stable, reliable, and will continue after your mortgage has closed. What some don’t realize about this process is that there are standards for verifying income.

April 1, 2023FHA loan rules for single family purchase loans include guidelines for the lender to use if the applicant has rental income. Some want to know whether it is possible to qualify for an FHA mortgage using rental income. The real issue is whether the rental income meets FHA loan rules.

March 16, 2023Planning your FHA loan means asking some important questions early in the process. The most obvious question is associated with the type of home you want. How large a house do you need? FHA mortgages allow the purchase of homes with between one and four living units.

February 7, 2023There are tons of reasons why people decide that they’re done with renting and start looking into buying a home. Whatever your reason, deciding to buy a home is a big step, and one of the most daunting aspects is saving up enough money for the down payment.

January 27, 2023Before you get ready to commit to a home loan application, it’s good to review your circumstances and ask a few basic questions about your loan, your plans, and the home itself. Believe it or not, knowing what type of home loan you need is an important step.