First-Time Homebuyer FAQs: Demystifying Mortgage Terms

February 26, 2025

I keep hearing about "principal" and "interest." What's the difference?

Think of it like this: the principal is the main dish – it's the actual amount of money you borrow from the lender to buy your home. The interest is like the extra side dishes and drinks you order. It's the cost of borrowing that principal amount. Interest is calculated as a percentage of the principal, and that percentage is your interest rate.

What does "loan term" mean, and why does it matter?

The loan term is simply the length of time you have to repay the mortgage, usually measured in years (e.g., 15 years, 30 years). It matters because a shorter term means higher monthly payments but less total interest paid over the life of the loan. A longer home loan term can bring lower monthly payments, but you'll end up paying more in interest over time.

How is my monthly payment determined?

Your mortgage payment is based on the principal, interest rate, and loan term. Part of that payment reduces the principal and there is a portion covering the interest. In the early years of your mortgage, more of your payment goes towards interest. Gradually, more and more goes towards paying down the principal.

What is amortization?

Amortization is just a fancy word for the process of gradually paying off your mortgage over time. An amortization schedule shows exactly how each monthly payment is divided between principal and interest, and how your loan balance decreases over the years.

What are the main types of mortgages I should know about?

There are several key types of mortgages. With a fixed-rate mortgage, your interest rate stays the same. It does not change during the loan term. This creates predictable monthly payments. In contrast, an adjustable-rate mortgage (ARM) has an interest rate that can change periodically, typically annually, which means your monthly payments can go up or down.

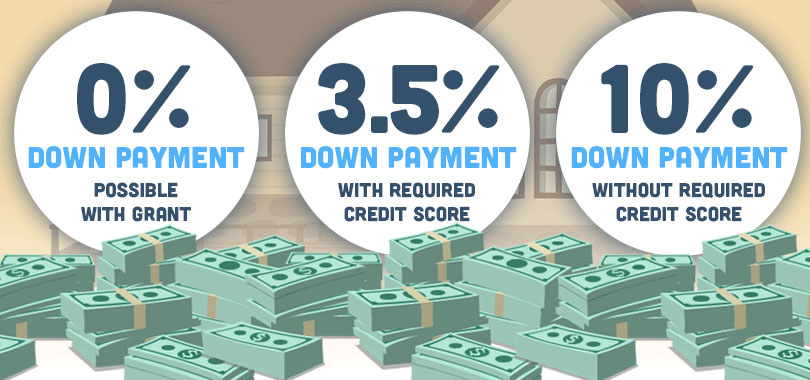

If you are a first-time homebuyer or have a lower credit score or smaller down payment, you might consider an FHA loan. These loans are insured by the Federal Housing Administration.

What are closing costs, and what do they include?

Closing costs are the various fees and expenses you pay to finalize your mortgage. They typically include things like a loan origination fee, an appraisal fee that covers the cost of assessing the property's value, title insurance, and recording fees paid to the government to record the sale.

What's the deal with mortgage insurance?

Mortgage insurance protects the lender. The insurance pays the lender if you default on the mortgage. For conventional loans, this is called Private Mortgage Insurance (PMI), while for FHA loans, it's called Mortgage Insurance Premium (MIP).

What is an escrow account?

An escrow account is like a holding pen for your property taxes and homeowners insurance payments. Your lender manages this account and uses it to pay those bills on your behalf, ensuring you stay current. Your mortgage payment may include money intended for escrow.

What are "prepaids" at closing?

Prepaids are upfront costs you cover at closing, such as prepaid interest, property taxes, and homeowners insurance premiums.

How does my credit score affect my mortgage?

Your FICO score is used to assess how risky it is to lend you money. A higher score generally means you'll qualify for a lower interest rate and better loan terms.

What does it mean to get pre-approved for a mortgage?

Getting pre-approved means a lender has reviewed your finances and given you an estimate of how much you can borrow. This is a smart move before house hunting because it shows sellers you're a serious buyer.

What are the Loan Estimate and Closing Disclosure?

These are important documents you'll receive during the mortgage process. The Loan Estimate provides an early estimate of your loan terms, interest rate, and closing costs, while the Closing Disclosure gives you the final details of your loan before you sign on the dotted line.

FHA Loan Articles

November 21, 2024The dream of homeownership is with some from a young age. But in an uncertain housing market, some grapple with the question: Is buying a home the right move for me?

While renting offers relocation flexibility and lower upfront costs, homeownership provides a wealth of financial and personal benefits.

November 20, 2024Refinancing your mortgage offers a way to cash in on your home equity, potentially reduce your interest rate, or modify your loan term. Borrowers ready to consider have options including FHA loans and conventional loans.

While both provide avenues for refinancing, each loan type may be best for specific needs and financial circumstances. What are the differences between FHA and conventional refinance options?

November 14, 2024The home you want to buy might seem perfect, or it may have a few flaws that are acceptable in the grand scheme of things. But what about issues you can’t spot just by walking through the property a few times? A home inspection provides an unbiased, expert assessment of the property's condition, uncovering potential issues that might not be noticeable to the untrained observer.

November 12, 2024Escrow is an important feature of most typical FHA loans. An escrow account is a third-party account where borrowers deposit funds designated for property taxes and other uses. Requirements to use escrow accounts typically stems from a need to protect all parties involved in the transaction

November 2, 2024When it’s time to consider buying a home, the Federal Housing Administration (FHA) offers two popular options. One is the traditional FHA purchase loan many use to buy a house in the suburbs. But not everyone wants to buy an existing property. Some want more control over the design and configuration of the home.

The other FHA construction loan option, the one-time close mortgage, comes in here. This option is for those who want to approve floor plans, have a say in the types of materials used to build the home and choose its features.