Graduated Payment Mortgage

The FHA has a particular loan available for low- to moderate-income homebuyers who expect their incomes to increase in upcoming years. The Graduated Payment Mortgage (GPM), also known as HUD's Section 245(a), is a kind of fixed-rate mortgage that starts with lower monthly payments that gradually increase based on a predefined schedule. Typically, the GPM payments increase between 7-12% annually from the initial amount until the full monthly payment amount is reached.

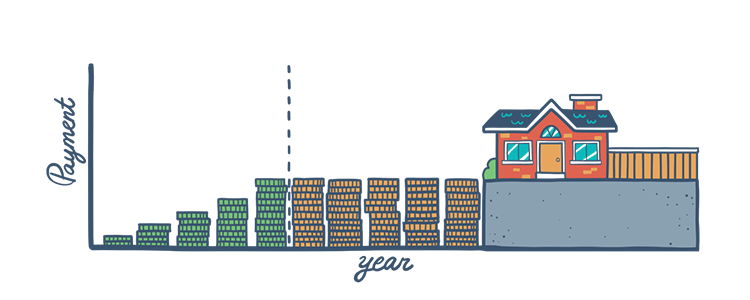

How Does a GPM Work?

It's important to understand how the monthly mortgage payments for a graduated payment mortgage work differently than that of a regular fixed-rate loan. A graduated payment mortgage starts with smaller minimum payments, with the payment amount increasing gradually over time. The low introductory interest rates make it so more borrowers—who might not otherwise qualify—can afford the low initial payments and be eligible for the loan. Different payment plans are available with varying lengths and rate of payment increases, and some include a higher down payment as well.

The FHA offers five different GPM plans to suit borrowers' needs.

- Plan I:

Monthly mortgage payments increase 2.5% each year for 5 years - Plan II:

Monthly mortgage payments increase 5% each year for 5 years - Plan III:

Monthly mortgage payments increase 7.5% each year for 5 years - Plan IV:

Monthly mortgage payments increase 2% each year for 10 years - Plan V:

Monthly mortgage payments increase 3% each year for 10 years

Once the loan reaches the set time period of rate increase, monthly payments remain constant for the remainder of the mortgage term. Keep in mind that borrowers must make higher monthly payments toward the end of the loan as they'll begin to pay down the deferred debt.

Who's it For?

FHA's graduated payment mortgage program is available to finance single-family homes which must serve as the borrower's primary residence. The loan is ideally suited for low- to moderate-income who see their income levels increasing over the coming years. Buyers can tailor the monthly mortgage payments by picking the best plan, giving themselves the means to purchase a home sooner than they would be able to through conventional financing programs. In addition to the payment plans, GPMs come with FHA's flexible eligibility requirements, including low down payments and credit scores.

GPM borrowers should understand that over the life of the mortgage, they will pay more in interest than they would have had they chosen a mortgage with payments that remained the same over the life of the loan. While this type of loan is a great way to purchase a home earlier instead of renting, potential borrowers should also be critical and honest when assessing their future income increments and job security.

FHA Loan Articles

February 7, 2023There are tons of reasons why people decide that they’re done with renting and start looking into buying a home. Whatever your reason, deciding to buy a home is a big step, and one of the most daunting aspects is saving up enough money for the down payment.

January 27, 2023Before you get ready to commit to a home loan application, it’s good to review your circumstances and ask a few basic questions about your loan, your plans, and the home itself. Believe it or not, knowing what type of home loan you need is an important step.

January 10, 2023When getting ready to shop for a home loan, it's worth taking a look at your credit report. Your credit score is a big factor when lenders take a look at your loan application, and it plays a huge role in the interest rate you get.

December 23, 2022When it comes to buying a house, saving up for a down payment can be one of the most overwhelming aspects. While down payments are one of the biggest obstacles for many in the mortgage process, it helps to understand the ins and outs of why they play such a big role.

November 30, 2022Buying and financing a home is complicated and can become overwhelming. It's important for you to stay informed, and know what your options are. So, start with the basics and read about the four different mortgage types available before approaching a lender.

November 8, 2022The fact is that repairs and renovations to your home cost a lot of money. Luckily, the FHA has an option for those with fixer-uppers on their hands. The FHA 203(k) Rehabilitation Mortgages allows borrowers to finance the funds for renovations to a home.