What Goes Into Escrow?

May 21, 2026

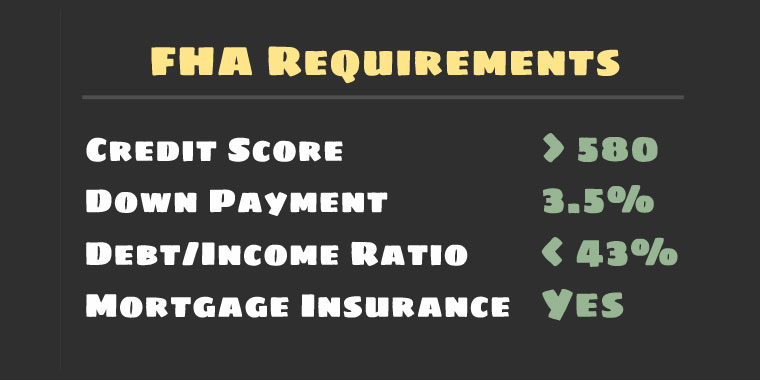

While some conventional loans may allow property owners to manage their own tax and insurance payments if they provide a down payment of 20 percent or more, the FHA loan program allows no exceptions or waivers, regardless of the size of your initial down payment.

How it Works

Your FHA lender divides your total annual property taxes and homeowners' insurance premiums into twelve equal installments. Your lender adds this amount to your base monthly payment of principal and interest.

When the annual bills for your taxes and insurance premiums are issued, the servicer draws directly from this accumulated cash reserve to pay the bills on your behalf.

What's Paid From Escrow

Local governments can place a tax lien on a home if property taxes go unpaid. This lien takes priority over the bank's mortgage, so naturally, your lender wants to avoid this and review your local tax assessment and bills accordingly.

Hazard insurance, to include your base homeowners insurance premium, which protects the physical structure against perils like fire, theft, and severe weather. The servicer manages this bill to ensure your coverage never lapses.

Properties located within a federally designated Special Flood Hazard Area require mandatory flood insurance, which is routed through the escrow account. Local government assessments for infrastructure improvements, such as neighborhood sewer lines or sidewalk repairs, which may also be funded through this account.

Housing Expenses Paid Outside Escrow

FHA loans require a Mortgage Insurance Premium. While this fee is collected alongside your monthly mortgage payment, the funds may enter your escrow account. The servicer may send them to the FHA to maintain the government insurance backing on the loan.

Fees required by a neighborhood association or a condominium board must be paid directly to the organization. Your FHA lender will not manage HOA fees through the escrow account, even though unpaid dues can result in property liens in certain states.

If the local tax assessor updates your property value they may issue a one-time supplemental tax bill to cover the value difference. These physical bills are mailed directly to your home and must be paid out of pocket, as they fall outside the standard annual tax cycle used to build your regular escrow account.

Funding Escrow

An FHA escrow account cannot start with a zero balance. You will put money in escrow on closing day, with your lender determining the number of months remaining before the next property tax and insurance bills are due.

Federal law allows lenders to maintain a financial safety net inside the account to protect against tax hikes or insurance premium increases. Ask your lender about this before you commit.

Property taxes and insurance premiums change over time and your payments may change over the years depending on circumstances. Your lender is required to do escrow analysis to compare their previous estimates against the actual bills paid over the past year.

FHA Loan Articles

June 30, 2026FHA loans offer low down payment options and more forgiving credit requirements for borrowers who may not qualify for a conventional mortgage or need to save more money out of pocket at the front end of the mortgage. But even with more forgiving credit requirements, some borrowers are tempted to omit certain debt information from their home loan applications. What does it mean to conceal a debt or financial situation from your loan officer?

June 30, 2026Some borrowers start working on their credit scores but get impatient with the process because they can't predict when their efforts will change their FICO scores. How long does it take for your FICO scores to update when you pay off a loan, reduce your credit card balances, or take other steps to make yourself a better credit risk? The short answer is that credit reporting procedures are not standardized, and it may take more time than you realize to get those positive credit actions added to your credit report.

June 29, 2026Mortgage interest rates are "moving targets" shaped by national economic trends and the borrower's specific financial profile. What is your FHA loan interest rate? Much depends on the financial data you bring to the table. Lenders set interest rates daily based on a snapshot of market conditions, but the rate ultimately offered also reflects risk, equity, and the lending institution's internal operational costs.

June 28, 2026An FHA appraisal differs from a conventional appraisal. While the goal of a conventional appraisal centers on market value, the FHA appraisal also focuses on the buyer's safety and soundness. FHA lenders select the appraiser, not the home buyer.

June 24, 2026FHA loan closing costs vary by property price and geographic location, rather than by a single nationwide flat fee. Total settlement charges combine percentage-based fees, local government taxes, and marketplace service costs. If you are new to buying a home, you'll want to get familiar with the closing cost issues discussed here to avoid budgetary surprises later on.