Getting to Know Credit Bureaus Before You Apply for an FHA Mortgage

March 24, 2026

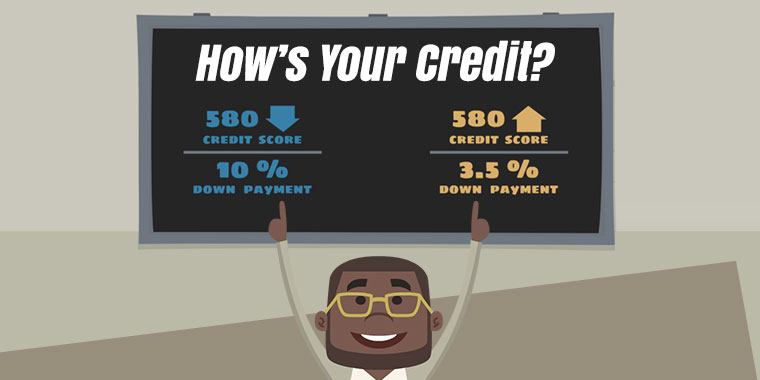

The roles of the three major credit bureaus and the evolution of credit scoring models are important to those buying a home, especially first-time home buyers. Knowing how credit bureaus work can help you better plan your home loan while you are still working on your credit and saving for your down payment.

Credit bureaus are not part of the federal government.

Equifax, Experian, and TransUnion are independent, publicly traded corporations. Although they are central to the American financial system, they operate as private businesses with multi-billion-dollar valuations rather than government agencies.

How Credit Bureaus obtain information about your financial habits.

The bureaus act as repositories for data provided by "furnishers." These include credit card issuers, student loan providers, and auto lenders. Because reporting is voluntary, a lender might send data to one bureau but not the others, which often leads to discrepancies between your different credit files.

What FHA lenders review during the application process.

Lenders typically pull a tri-merge credit report. This report provides a comprehensive overview by simultaneously pulling and consolidating data from all three major bureaus. It ensures the lender sees a complete picture of your credit history across the entire industry.

Credit scores an FHA lender uses if the three bureaus report different numbers.

Lenders generally rely on the middle score. For an applicant with scores of 620, 640, and 650, the qualifying score would be 640. In cases involving a co-borrower, the lender typically identifies the middle score for each person and then uses the lower of those two figures to evaluate the loan.

What is the difference between a credit bureau and FICO?

The bureaus are the libraries that store your data, while FICO is the mathematician who analyzes it. The Fair Isaac Corporation develops the proprietary algorithms used to estimate the likelihood that a borrower will fall 90 days behind on payments. Their "Classic FICO" model has served as the industry standard for nearly three decades.

How the mortgage industry updated its scoring methods in 2026.

The market is currently transitioning to more inclusive models like VantageScore 4.0 and FICO 10T. This shift is meant to help first-time buyers who have limited credit histories. Unlike older versions, these models can factor in "alternative" data, such as a consistent record of paying rent, phone bills, and utilities.

What is "trended data" and why does it matter for a home loan?

Trended data is a feature of the newest scoring models that looks at the trajectory of your debt over time. Instead of viewing a single snapshot of your current balances, the system analyzes whether your debt is shrinking or growing. This provides a more accurate reflection of your financial trajectory and management habits.

How does VantageScore differ from the FICO model?

While FICO is an independent company, VantageScore was developed as a joint venture among Equifax, Experian, and TransUnion. Both companies now compete to provide the scoring formulas used in the FHA mortgage process.

FHA Loan Articles

June 30, 2026FHA loans offer low down payment options and more forgiving credit requirements for borrowers who may not qualify for a conventional mortgage or need to save more money out of pocket at the front end of the mortgage. But even with more forgiving credit requirements, some borrowers are tempted to omit certain debt information from their home loan applications. What does it mean to conceal a debt or financial situation from your loan officer?

June 30, 2026Some borrowers start working on their credit scores but get impatient with the process because they can't predict when their efforts will change their FICO scores. How long does it take for your FICO scores to update when you pay off a loan, reduce your credit card balances, or take other steps to make yourself a better credit risk? The short answer is that credit reporting procedures are not standardized, and it may take more time than you realize to get those positive credit actions added to your credit report.

June 29, 2026Mortgage interest rates are "moving targets" shaped by national economic trends and the borrower's specific financial profile. What is your FHA loan interest rate? Much depends on the financial data you bring to the table. Lenders set interest rates daily based on a snapshot of market conditions, but the rate ultimately offered also reflects risk, equity, and the lending institution's internal operational costs.

June 28, 2026An FHA appraisal differs from a conventional appraisal. While the goal of a conventional appraisal centers on market value, the FHA appraisal also focuses on the buyer's safety and soundness. FHA lenders select the appraiser, not the home buyer.

June 24, 2026FHA loan closing costs vary by property price and geographic location, rather than by a single nationwide flat fee. Total settlement charges combine percentage-based fees, local government taxes, and marketplace service costs. If you are new to buying a home, you'll want to get familiar with the closing cost issues discussed here to avoid budgetary surprises later on.