FHA Loans When You Have A Bankruptcy on Your Credit Record

February 24, 2026

These mandatory waiting periods, required by the FHA, ensure that a borrower has demonstrated financial recovery before taking on a new government-backed loan. Here's what you need to know before you start applying for a new loan after you are free to do so.

Waiting Period for a Chapter 7 Bankruptcy

For a Chapter 7 liquidation, the standard waiting period is two years from the date of your discharge. It is important to note that this clock starts at the discharge date, not the initial filing date. During this two-year window, you must demonstrate that you have managed all financial obligations without any new derogatory credit.

Exceptions to the Two-Year Period for Chapter 7

The FHA may allow an exception to the two-year rule in rare circumstances, potentially reducing the wait to 12 months. These exceptions are handled on a case-by-case basis and typically require documentation of a one-time event beyond the borrower's control that led to the filing.

Chapter 13 Bankruptcy

FHA guidelines for Chapter 13 are more flexible because the process involves a court-ordered repayment plan. You may qualify for an FHA loan after 12 months of your repayment plan, if all payments were made on time.

If the Chapter 13 has already been discharged, the FHA does not require an additional waiting period, though individual lenders may apply their own stricter internal rules.

If you are currently in a Chapter 13 repayment plan, obtain written permission from the bankruptcy court or the trustee to enter into a new mortgage transaction.

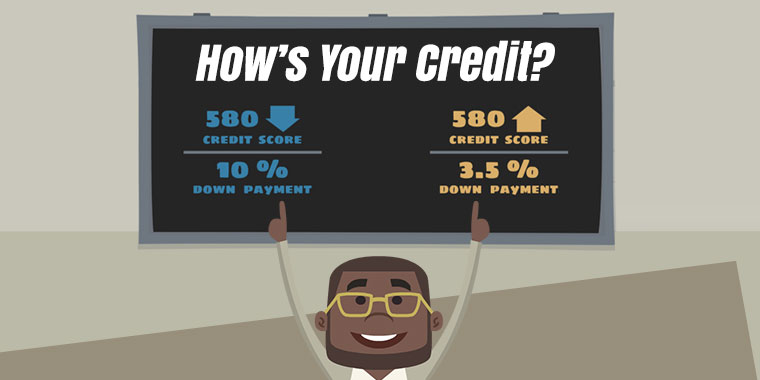

Credit Scores Required for an FHA Loan After Bankruptcy

To qualify for the 3.5% down payment program, a borrower must have a FICO score of at 580 or better. Additional lender standards may apply.

Best Ways to Rebuild Credit

Effective strategies include using secured credit cards to create a pattern of on-time payments. Maintain a history of on-time rent or mortgage payments. Avoid opening high-interest retail accounts immediately after a discharge. Lenders view this unfavorably.

You must provide your lender with a complete bankruptcy package, including all schedules and the final discharge notice. Additionally, you will need standard financial documents such as tax returns, W-2s, and bank statements.

The Letter of Explanation

This is a factual, concise document that describes the specific cause of the bankruptcy, such as a medical crisis or job loss. The letter must also detail the steps you have taken to improve your financial stability and explain why the issues that led to the bankruptcy are unlikely to recur.

FHA Loan Income and Employment Requirements

Borrowers should generally show at least two years of stable employment or a consistent history in the same field.

FHA debt-to-income (DTI) ratios are typically limited to 43%, though lenders may allow higher ratios if you have large cash reserves or other compensating factors.

Prepare for the Application Process

Review your credit reports from all three bureaus to ensure the bankruptcy is accurately marked as "discharged" and that no old debts remain active. Ensuring your credit report is up to date is a vital step before contacting a lender.

FHA Loan Articles

June 30, 2026FHA loans offer low down payment options and more forgiving credit requirements for borrowers who may not qualify for a conventional mortgage or need to save more money out of pocket at the front end of the mortgage. But even with more forgiving credit requirements, some borrowers are tempted to omit certain debt information from their home loan applications. What does it mean to conceal a debt or financial situation from your loan officer?

June 30, 2026Some borrowers start working on their credit scores but get impatient with the process because they can't predict when their efforts will change their FICO scores. How long does it take for your FICO scores to update when you pay off a loan, reduce your credit card balances, or take other steps to make yourself a better credit risk? The short answer is that credit reporting procedures are not standardized, and it may take more time than you realize to get those positive credit actions added to your credit report.

June 29, 2026Mortgage interest rates are "moving targets" shaped by national economic trends and the borrower's specific financial profile. What is your FHA loan interest rate? Much depends on the financial data you bring to the table. Lenders set interest rates daily based on a snapshot of market conditions, but the rate ultimately offered also reflects risk, equity, and the lending institution's internal operational costs.

June 28, 2026An FHA appraisal differs from a conventional appraisal. While the goal of a conventional appraisal centers on market value, the FHA appraisal also focuses on the buyer's safety and soundness. FHA lenders select the appraiser, not the home buyer.

June 24, 2026FHA loan closing costs vary by property price and geographic location, rather than by a single nationwide flat fee. Total settlement charges combine percentage-based fees, local government taxes, and marketplace service costs. If you are new to buying a home, you'll want to get familiar with the closing cost issues discussed here to avoid budgetary surprises later on.