How FHA Loan Rules Protect Your Investment

January 29, 2026

Some of the FHA loan rules also protect the lender from loans that are too risky, and while that might seem irrelevant from a consumer point of view, in a backhanded way, these lender guidelines also protect the consumer, typically in the form of keeping someone who can't truly afford the loan from committing to it.

The FHA loan regulations that protect the borrower are a safety net helping you to avoid purchasing a home that won't be worth what you paid for it by the time you sell or refinance.

While many buyers view the appraisal and underwriting process as a hurdle, these steps exist to prevent you from inheriting a disaster. FHA loan rules that protect consumers focus on the property's condition and the sustainability of the FHA loan debt.

The FHA Loan Amendatory Clause

The FHA Amendatory Clause provides financial protection right from the start of the transaction. This clause states that you have no obligation to complete the sale if the appraisal value comes in lower than the asking price.

If the appraiser determines the house is worth less than the amount you agreed to pay, you can cancel the deal without penalty, since the law requires the lender to return your earnest money deposit in this situation.

This FHA loan rule prevents you from overpaying for a property and protects your cash. It also prevents the lender from giving you a loan for more than the value of the collateral.

FHA Property Standards

The FHA establishes Minimum Property Requirements (MPRs) for homes purchased with FHA mortgages. These standards must be met, or the home must be brought into compliance as a condition of FHA loan approval.

One MPR involves lead paint in homes built before 1978. If the appraiser observes chipping or peeling paint, the seller must scrape and repaint those surfaces, as the FHA presumes there is lead-based paint.

The FHA also requires a water supply inspection to ensure it is clean. If the home uses a well, the well water must be tested for bacteria or chemicals. The appraiser also verifies that the sewage system is leak-free.

The FHA requires the roof to be in good repair; it must prevent moisture from entering the house. If the roof shows signs of failure, the seller must correct it before you buy the house. These rules and others like it ensure that the house remains a durable asset.

Underwriting Ratios

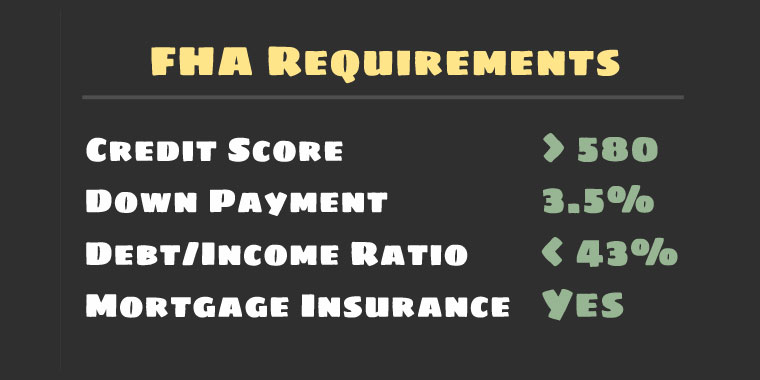

The lender reviews your income and your bills to determine your debt-to-income ratio, and while not technically a consumer protection this practice prevents the lender from approving loans that potential borrowers can't realistically afford. Yes, this protects the lender first, but borrowers should know why the FHA enforces such guidelines.

FHA typically limits the house payment to 31 percent of your gross income. The total debt ratio, which includes car payments and credit card debt, is typically 43 percent. These limits prevent you from becoming "house poor."

The FHA also tracks the source of your down payment, typically to make sure the money is from approved sources and not from loans disguised as gifts. If you receive a downpayment gift, the lender must document it to prove you do not owe more money to a third party. These rules build a foundation for your financial success as a homeowner.

Foreclosure Prevention

The FHA provides protections that continue after you sign the papers. If you face a hardship, such as a job loss or illness, the FHA requires the lender to assist. The lender must contact you to discuss options to avoid foreclosure. These options include forbearances and repayment plans.

The FHA offers a Partial Claim program in which the government pays the lender for missed payments. You pay the government back when you sell the house or finish the loan, helping your family stay in the home during a financial crisis. The lender can also modify the loan to lower the interest rate or extend the term.

FHA Loan Articles

June 30, 2026FHA loans offer low down payment options and more forgiving credit requirements for borrowers who may not qualify for a conventional mortgage or need to save more money out of pocket at the front end of the mortgage. But even with more forgiving credit requirements, some borrowers are tempted to omit certain debt information from their home loan applications. What does it mean to conceal a debt or financial situation from your loan officer?

June 30, 2026Some borrowers start working on their credit scores but get impatient with the process because they can't predict when their efforts will change their FICO scores. How long does it take for your FICO scores to update when you pay off a loan, reduce your credit card balances, or take other steps to make yourself a better credit risk? The short answer is that credit reporting procedures are not standardized, and it may take more time than you realize to get those positive credit actions added to your credit report.

June 29, 2026Mortgage interest rates are "moving targets" shaped by national economic trends and the borrower's specific financial profile. What is your FHA loan interest rate? Much depends on the financial data you bring to the table. Lenders set interest rates daily based on a snapshot of market conditions, but the rate ultimately offered also reflects risk, equity, and the lending institution's internal operational costs.

June 28, 2026An FHA appraisal differs from a conventional appraisal. While the goal of a conventional appraisal centers on market value, the FHA appraisal also focuses on the buyer's safety and soundness. FHA lenders select the appraiser, not the home buyer.

June 24, 2026FHA loan closing costs vary by property price and geographic location, rather than by a single nationwide flat fee. Total settlement charges combine percentage-based fees, local government taxes, and marketplace service costs. If you are new to buying a home, you'll want to get familiar with the closing cost issues discussed here to avoid budgetary surprises later on.