Credit Basics For FHA Home Loan Approval

September 23, 2025

FHA sets the minimum guidelines, but individual lenders have their own rules that also must be considered.

The following questions and answers break down these requirements. We cover the FHA's official credit score tiers, the impact of lender-specific rules, and how major events like bankruptcy or foreclosure are treated.

What is the minimum credit score for an FHA loan?

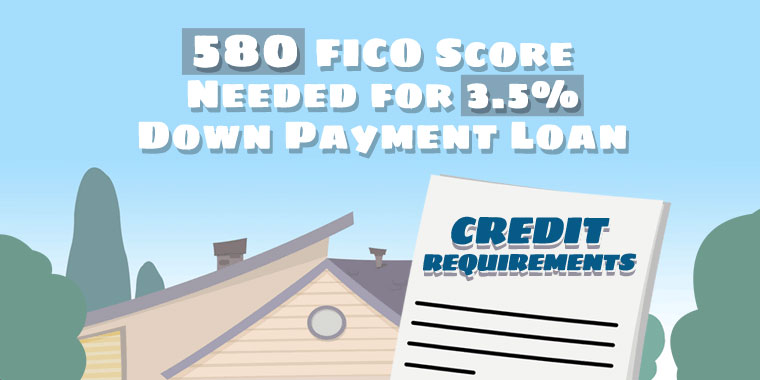

The FHA has two main credit score tiers. A score of 580 or higher qualifies you for the minimum 3.5 percent down payment. If your score is between 500 and 579, you may still qualify but will be required to make a larger down payment of at least 10 percent. Scores below 500 are generally not eligible.

Why did a lender tell me I need a 620 score if the FHA minimum is 580?

This is due to "lender overlays." Lenders can impose their own requirements on top of the FHA's minimums to reduce their risk. Because these overlays vary, it is a good idea to apply with more than one lender.

Can I get an FHA loan if I don't have a credit score?

If you do not have a traditional credit history, the FHA allows lenders to perform "manual underwriting." This involves evaluating your financial history using other sources.

What is non-traditional credit?

Non-traditional credit is a history of on-time payments for recurring bills. For an FHA loan, lenders can consider a 12-month history of payments for things like rent, utilities (gas, electric), insurance premiums, and phone bills to establish your creditworthiness.

How long do I have to wait after a bankruptcy?

For a Chapter 7 bankruptcy, there is typically a two-year waiting period from the discharge date. For a Chapter 13 bankruptcy, you may qualify after making 12 months of on-time payments with the court's permission.

Is there a waiting period after a foreclosure?

Yes, there is generally a three-year waiting period from the date the property deed was transferred out of your name.

Are there exceptions to these waiting periods?

Shorter waiting periods may be possible if you can prove the bankruptcy or foreclosure was caused by an extenuating circumstance beyond your control, such as a serious illness. You must also show that you have re-established good credit.

How important is my recent credit history?

It is extremely important. Lenders focus heavily on your credit behavior in the last 12 to 24 months. A recent history of on-time payments and financial stability is a critical factor for approval.

How do student loans affect my FHA application?

Lenders must include a monthly student loan payment in your debt-to-income ratio. Even if your loans are in deferment or forbearance, the lender will typically use 0.5 percent of the outstanding loan balance as your monthly payment for qualification purposes.

Do collections on my credit report need to be paid off?

It depends. FHA guidelines do not require medical collection accounts to be paid off. For non-medical collections totaling over $2,000, the lender may require you to either pay them off or set up a payment plan, and that monthly payment will be included in your debts.

Does my spouse's bad credit affect my application?

If you are the only applicant for the loan, your non-borrowing spouse's credit score is not considered for qualification purposes. However, if you live in a community property state, your spouse's debts will generally be included in your debt-to-income calculation, even if they are not on the loan.

What should I avoid doing right before applying for a loan?

In the months leading up to your application, you should avoid several actions. Do not open new credit cards or take out new loans. Do not make large, undocumented cash deposits into your bank accounts. Do not change jobs, and refrain from co-signing a loan for anyone else. Any of these actions can complicate or delay your loan approval.

FHA Loan Articles

June 30, 2026FHA loans offer low down payment options and more forgiving credit requirements for borrowers who may not qualify for a conventional mortgage or need to save more money out of pocket at the front end of the mortgage. But even with more forgiving credit requirements, some borrowers are tempted to omit certain debt information from their home loan applications. What does it mean to conceal a debt or financial situation from your loan officer?

June 30, 2026Some borrowers start working on their credit scores but get impatient with the process because they can't predict when their efforts will change their FICO scores. How long does it take for your FICO scores to update when you pay off a loan, reduce your credit card balances, or take other steps to make yourself a better credit risk? The short answer is that credit reporting procedures are not standardized, and it may take more time than you realize to get those positive credit actions added to your credit report.

June 29, 2026Mortgage interest rates are "moving targets" shaped by national economic trends and the borrower's specific financial profile. What is your FHA loan interest rate? Much depends on the financial data you bring to the table. Lenders set interest rates daily based on a snapshot of market conditions, but the rate ultimately offered also reflects risk, equity, and the lending institution's internal operational costs.

June 28, 2026An FHA appraisal differs from a conventional appraisal. While the goal of a conventional appraisal centers on market value, the FHA appraisal also focuses on the buyer's safety and soundness. FHA lenders select the appraiser, not the home buyer.

June 24, 2026FHA loan closing costs vary by property price and geographic location, rather than by a single nationwide flat fee. Total settlement charges combine percentage-based fees, local government taxes, and marketplace service costs. If you are new to buying a home, you'll want to get familiar with the closing cost issues discussed here to avoid budgetary surprises later on.