How's Your Credit, House Hunter?

May 30, 2025

How long does it typically take for a house hunter to get their credit ready for an FHA home loan?

The exact timeframe varies. When that data is pulled, your credit report is meant to examine your current financial situation. If you need to improve your credit score in a major way, it will take time for your improved credit habits to be listed in your credit report.

Generally, house hunters should expect the process to take anywhere from a few months to over a year. For minor adjustments, a few months might suffice. For a major credit rebuild the process can extend beyond a year, sometimes even several years.

This duration is directly linked to the current state of one's credit and the diligence applied to improving it.

What are the main factors that determine a credit score, and how do they impact the timeline for credit readiness?

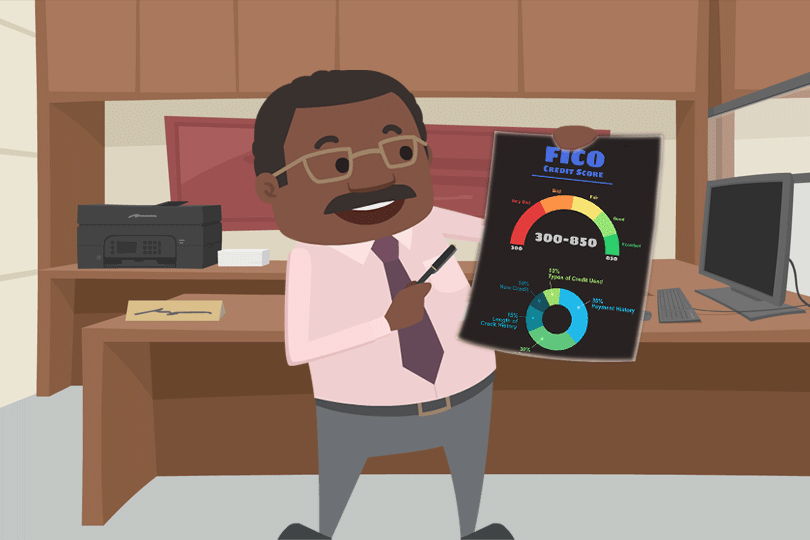

Multiple factors go into a credit score, each playing a crucial role. Payment history is the most important. Consistent, on-time payments are the key to good credit. Any missed payment can potentially damage your scores for up to seven years. Therefore, if there's a history of late payments, establishing a perfect record is the first and most time-consuming step for recovery.

Credit utilization is another big factor. The lender must measure how much of your available credit you are using. High credit card balances may hurt your scores even if paid on time. Reducing these balances may show results within a month or two, as balances are reported monthly, but your experience may vary.

Length of credit history is another consideration. The lender wants to know how long your accounts have been open. This factor simply takes time to build; there are no shortcuts. For those new to credit, a score generally takes at least six months of account activity to generate.

Borrower beware: too many applications for new credit could (temporarily) lower your score due to "hard inquiries." Avoid new credit applications, especially before a mortgage application. This will help prevent unnecessary delays.

Finally, the variety of your credit accounts matters. A diverse mix can be positive, but one should not open new accounts solely for this purpose if it means taking on unnecessary debt or hard inquiries.

What is my first step if I have a history of missed payments?

Establish a perfect record of timely payments on all your debts. This includes credit cards, car loans, student loans, and other financial obligations. You must ensure every single payment is made by its due date, without exception. This consistent, positive behavior is the most influential factor in your credit score and will gradually lead to recovery, though it takes time for the full effect to show.

How quickly can reducing credit card balances impact my credit score?

Reducing your credit card balances, particularly lowering your credit utilization ratio, can have a faster impact on your credit score. Since credit card companies typically report balances to the credit bureaus on a monthly basis, you might see an improvement in your score within just a month or two after aggressively paying down high balances. The goal is to use less than thirty percent of your total available credit, with ten percent or less ideal for optimal results.

What should I do if I have little to no credit history?

If you have little to no credit history, building it takes time. A FICO score typically requires at least six months of activity on one or more accounts to generate. The best approach is to open a few manageable credit accounts, such as a secured credit card or a small installment loan, and then consistently make all payments on time. The key is patience, as the length of your credit history factor grows over time.

What is the benefit of getting my credit reports long before a mortgage application?

Obtaining and meticulously reviewing your credit reports from all three major bureaus (Experian, Equifax, and TransUnion) well in advance is a crucial practical step. This allows you to identify any errors or inaccuracies. Look for incorrect personal information, accounts that do not belong to you, or outdated negative entries.

Disputing these errors promptly with the credit bureaus can lead to a quicker and often significant improvement in your score, as they are legally required to investigate and correct inaccuracies, usually within thirty days. Catching and correcting these issues early can save you significant time and stress later in the home loan process.

Will applying for multiple new lines of credit affect my credit score negatively?

The answer is typically yes. Applying for multiple new lines of credit quickly can negatively affect your credit score. Lenders may interpret a sudden rush of applications as a sign of financial trouble. It's best to avoid unnecessary credit applications in the months before a mortgage application. However, when shopping for a mortgage, multiple inquiries within a short window are often treated as a single inquiry to allow for rate comparison.

How quickly do changes to my credit activities, like paying down debt, show up on my credit report?

Credit score changes are not instantaneous. Lenders and credit card companies report information to the credit bureaus monthly. Therefore, the positive effects of diligently paying down debt or making on-time payments will accumulate over time.

You typically won't see an overnight transformation, but a gradual improvement will be reflected in your score as these monthly updates occur. While rapid rescore services exist for urgent situations, they are not a substitute for good financial habits.

FHA Loan Articles

June 30, 2026FHA loans offer low down payment options and more forgiving credit requirements for borrowers who may not qualify for a conventional mortgage or need to save more money out of pocket at the front end of the mortgage. But even with more forgiving credit requirements, some borrowers are tempted to omit certain debt information from their home loan applications. What does it mean to conceal a debt or financial situation from your loan officer?

June 30, 2026Some borrowers start working on their credit scores but get impatient with the process because they can't predict when their efforts will change their FICO scores. How long does it take for your FICO scores to update when you pay off a loan, reduce your credit card balances, or take other steps to make yourself a better credit risk? The short answer is that credit reporting procedures are not standardized, and it may take more time than you realize to get those positive credit actions added to your credit report.

June 29, 2026Mortgage interest rates are "moving targets" shaped by national economic trends and the borrower's specific financial profile. What is your FHA loan interest rate? Much depends on the financial data you bring to the table. Lenders set interest rates daily based on a snapshot of market conditions, but the rate ultimately offered also reflects risk, equity, and the lending institution's internal operational costs.

June 28, 2026An FHA appraisal differs from a conventional appraisal. While the goal of a conventional appraisal centers on market value, the FHA appraisal also focuses on the buyer's safety and soundness. FHA lenders select the appraiser, not the home buyer.

June 24, 2026FHA loan closing costs vary by property price and geographic location, rather than by a single nationwide flat fee. Total settlement charges combine percentage-based fees, local government taxes, and marketplace service costs. If you are new to buying a home, you'll want to get familiar with the closing cost issues discussed here to avoid budgetary surprises later on.