First-Time Homebuyer FAQs: Demystifying Mortgage Terms

February 26, 2025

I keep hearing about "principal" and "interest." What's the difference?

Think of it like this: the principal is the main dish – it's the actual amount of money you borrow from the lender to buy your home. The interest is like the extra side dishes and drinks you order. It's the cost of borrowing that principal amount. Interest is calculated as a percentage of the principal, and that percentage is your interest rate.

What does "loan term" mean, and why does it matter?

The loan term is simply the length of time you have to repay the mortgage, usually measured in years (e.g., 15 years, 30 years). It matters because a shorter term means higher monthly payments but less total interest paid over the life of the loan. A longer home loan term can bring lower monthly payments, but you'll end up paying more in interest over time.

How is my monthly payment determined?

Your mortgage payment is based on the principal, interest rate, and loan term. Part of that payment reduces the principal and there is a portion covering the interest. In the early years of your mortgage, more of your payment goes towards interest. Gradually, more and more goes towards paying down the principal.

What is amortization?

Amortization is just a fancy word for the process of gradually paying off your mortgage over time. An amortization schedule shows exactly how each monthly payment is divided between principal and interest, and how your loan balance decreases over the years.

What are the main types of mortgages I should know about?

There are several key types of mortgages. With a fixed-rate mortgage, your interest rate stays the same. It does not change during the loan term. This creates predictable monthly payments. In contrast, an adjustable-rate mortgage (ARM) has an interest rate that can change periodically, typically annually, which means your monthly payments can go up or down.

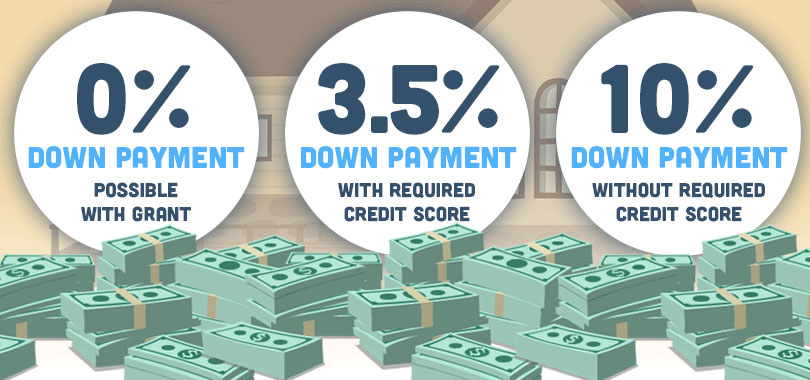

If you are a first-time homebuyer or have a lower credit score or smaller down payment, you might consider an FHA loan. These loans are insured by the Federal Housing Administration.

What are closing costs, and what do they include?

Closing costs are the various fees and expenses you pay to finalize your mortgage. They typically include things like a loan origination fee, an appraisal fee that covers the cost of assessing the property's value, title insurance, and recording fees paid to the government to record the sale.

What's the deal with mortgage insurance?

Mortgage insurance protects the lender. The insurance pays the lender if you default on the mortgage. For conventional loans, this is called Private Mortgage Insurance (PMI), while for FHA loans, it's called Mortgage Insurance Premium (MIP).

What is an escrow account?

An escrow account is like a holding pen for your property taxes and homeowners insurance payments. Your lender manages this account and uses it to pay those bills on your behalf, ensuring you stay current. Your mortgage payment may include money intended for escrow.

What are "prepaids" at closing?

Prepaids are upfront costs you cover at closing, such as prepaid interest, property taxes, and homeowners insurance premiums.

How does my credit score affect my mortgage?

Your FICO score is used to assess how risky it is to lend you money. A higher score generally means you'll qualify for a lower interest rate and better loan terms.

What does it mean to get pre-approved for a mortgage?

Getting pre-approved means a lender has reviewed your finances and given you an estimate of how much you can borrow. This is a smart move before house hunting because it shows sellers you're a serious buyer.

What are the Loan Estimate and Closing Disclosure?

These are important documents you'll receive during the mortgage process. The Loan Estimate provides an early estimate of your loan terms, interest rate, and closing costs, while the Closing Disclosure gives you the final details of your loan before you sign on the dotted line.

FHA Loan Articles

January 22, 2025Consider this scenario: you've been in your home for five years or more and you've likely built up a significant amount of equity, and now you might be wondering how to put that equity to work for you. Whether you're dreaming of a major renovation, need to consolidate debt, or want to help a child with college tuition, you have options. Two choices are an FHA cash-out refinance and a home equity line of credit (HELOC).

January 20, 2025The FHA Streamline Refinance offers a refinance option for those who don't want to cash in on their property's equity but instead want a lower payment or interest rate or who need to get out of an adjustable-rate mortgage. This streamlined program, designed specifically for those already in an FHA-insured mortgage, simplifies the refinancing process with fewer requirements and faster approval times depending on the transaction.

January 16, 2025Want to buy a home and thinking about getting an FHA loan? FHA loans are a great way to make homeownership happen, especially if you're a first-time buyer or don't have perfect credit. But you might wonder, "Can I get more than one FHA loan?"

The short answer is, it's tricky. The FHA itself doesn't say no automatically to having more than one loan. But there's a caveat. FHA loans are about helping you buy a place to live in – your main home base. Because of this, and a few other things, getting multiple FHA loans isn't easy.

January 15, 2025Buying a condo with an FHA loan is an option some don’t consider initially, but it’s worth adding to your list of potential property types. FHA loans for condo units traditionally require condo projects to be on or added to the FHA-approved list. Still, changes in policy over the years allow borrowers to apply for FHA loans on condo units in projects not on the list on a case-by-case basis.

December 30, 2024When applying for an FHA loan, lenders will consider more than just your credit scores and history. They also look at other factors affecting your risk profile and the interest rate they offer you.

One factor is occupancy type. For FHA loans, this is straightforward because these loans require owner occupancy. Investment properties aren't eligible. While conventional loans may have different rates for primary residences, second homes, and investment properties, this isn't a concern with FHA loans.