First-Time Homebuyer FAQs: Demystifying Mortgage Terms

February 26, 2025

I keep hearing about "principal" and "interest." What's the difference?

Think of it like this: the principal is the main dish – it's the actual amount of money you borrow from the lender to buy your home. The interest is like the extra side dishes and drinks you order. It's the cost of borrowing that principal amount. Interest is calculated as a percentage of the principal, and that percentage is your interest rate.

What does "loan term" mean, and why does it matter?

The loan term is simply the length of time you have to repay the mortgage, usually measured in years (e.g., 15 years, 30 years). It matters because a shorter term means higher monthly payments but less total interest paid over the life of the loan. A longer home loan term can bring lower monthly payments, but you'll end up paying more in interest over time.

How is my monthly payment determined?

Your mortgage payment is based on the principal, interest rate, and loan term. Part of that payment reduces the principal and there is a portion covering the interest. In the early years of your mortgage, more of your payment goes towards interest. Gradually, more and more goes towards paying down the principal.

What is amortization?

Amortization is just a fancy word for the process of gradually paying off your mortgage over time. An amortization schedule shows exactly how each monthly payment is divided between principal and interest, and how your loan balance decreases over the years.

What are the main types of mortgages I should know about?

There are several key types of mortgages. With a fixed-rate mortgage, your interest rate stays the same. It does not change during the loan term. This creates predictable monthly payments. In contrast, an adjustable-rate mortgage (ARM) has an interest rate that can change periodically, typically annually, which means your monthly payments can go up or down.

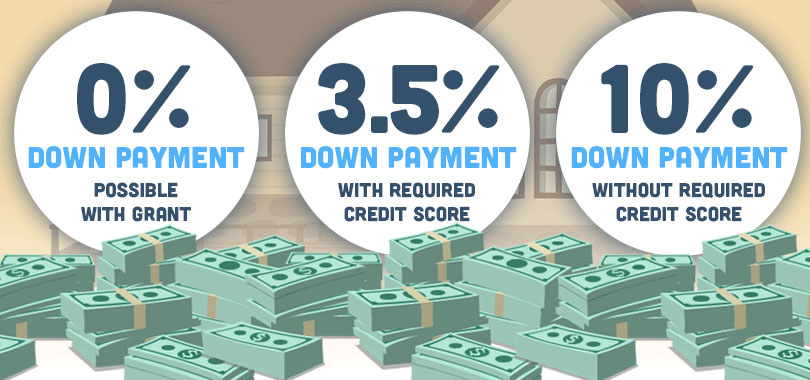

If you are a first-time homebuyer or have a lower credit score or smaller down payment, you might consider an FHA loan. These loans are insured by the Federal Housing Administration.

What are closing costs, and what do they include?

Closing costs are the various fees and expenses you pay to finalize your mortgage. They typically include things like a loan origination fee, an appraisal fee that covers the cost of assessing the property's value, title insurance, and recording fees paid to the government to record the sale.

What's the deal with mortgage insurance?

Mortgage insurance protects the lender. The insurance pays the lender if you default on the mortgage. For conventional loans, this is called Private Mortgage Insurance (PMI), while for FHA loans, it's called Mortgage Insurance Premium (MIP).

What is an escrow account?

An escrow account is like a holding pen for your property taxes and homeowners insurance payments. Your lender manages this account and uses it to pay those bills on your behalf, ensuring you stay current. Your mortgage payment may include money intended for escrow.

What are "prepaids" at closing?

Prepaids are upfront costs you cover at closing, such as prepaid interest, property taxes, and homeowners insurance premiums.

How does my credit score affect my mortgage?

Your FICO score is used to assess how risky it is to lend you money. A higher score generally means you'll qualify for a lower interest rate and better loan terms.

What does it mean to get pre-approved for a mortgage?

Getting pre-approved means a lender has reviewed your finances and given you an estimate of how much you can borrow. This is a smart move before house hunting because it shows sellers you're a serious buyer.

What are the Loan Estimate and Closing Disclosure?

These are important documents you'll receive during the mortgage process. The Loan Estimate provides an early estimate of your loan terms, interest rate, and closing costs, while the Closing Disclosure gives you the final details of your loan before you sign on the dotted line.

FHA Loan Articles

March 11, 2025Adding a co-borrower to your FHA is a way to offset fears that you won't qualify for the mortgage on your own. An FHA loan co-borrower with a more substantial financial profile may offset the primary borrower's weaknesses, demonstrating a reduced risk to the lender. But for an FHA loan, don't assume that one borrower with good credit scores can offset one with non-qualifying scores. We ask 20 questions about co-borrowing to help you better plan for your FHA loan.

March 10, 2025Even if you aren’t considering your home loan options right this second, it’s smart to know your options if you decide to pursue a new home later. To that end, using a mortgage calculator is a smart choice for setting some basic budgeting parameters as you plan your path toward home ownership. A mortgage calculator helps you plan for future financial scenarios, such as buying new or refinancing a current home.

February 27, 2025 Buying your first home can feel overwhelming, especially when you start hearing terms like "subprime mortgages" and "FHA loans." Understanding these options is crucial for making the right decision. Subprime mortgages are designed for borrowers with less-than-perfect credit histories. This might include past issues like late payments, loan defaults, or even bankruptcy...

February 26, 2025Buying your first home can be exciting, but the mortgage process often throws a curveball of unfamiliar terms. Here are answers to common questions first-time homebuyers have about mortgage jargon and terms.

February 18, 2025Mortgages typically require mortgage insurance and homeowners insurance. They are both key parts of your home loan but they serve very different functions. Do you know the differences between the two? Find out how ready you are to begin the process of buying your new house.