Frequently Asked Questions About Home Insurance with an FHA Mortgage

May 14, 2025

There are important nuances to these insurance policies to know before you start. What's the difference between insurance against water damage and flood insurance? As we'll explore below, that's just one example of the "hidden" expenses of buying your new home to budget for.

What kinds of insurance do I need when buying a house with an FHA mortgage?

If you purchase a home using an FHA residential real estate mortgage, you will primarily need to have FHA Mortgage Insurance Premium (MIP) and homeowner's insurance. Additionally, depending on your circumstances and the location of your property, you might need other types of insurance for full protection.

The FHA Mortgage Insurance Premium, or MIP, is a type of insurance that protects the lender against financial loss if you, the borrower, default on your loan. It helps make FHA loans available to a wider range of people.

What are the different parts of the FHA MIP?

The FHA MIP has two parts: the Upfront Mortgage Insurance Premium (UFMIP) and the Annual Mortgage Insurance Premium (Annual MIP).

What is the Upfront Mortgage Insurance Premium (UFMIP)?

The UFMIP is a one-time fee that you typically pay when you close on your house. It is usually a percentage of your total loan amount. While you can pay it in cash at closing, it's also common to add it to your loan balance.

What is the Annual Mortgage Insurance Premium (Annual MIP)?

The Annual MIP is an ongoing monthly payment that you make as part of your regular mortgage payment. The amount you pay depends on your loan amount, the length of your loan, and the size of your down payment.

Why do I have to pay the FHA Mortgage Insurance Premium?

The FHA MIP is required because FHA loans are designed to help people who might not qualify for traditional loans, often those with lower down payments or less-than-perfect credit. The MIP reduces the risk for lenders, allowing them to offer these loans.

What is homeowner's insurance (hazard insurance)?

Homeowner's insurance, often called hazard insurance when talking about mortgages, is another type of insurance you must have with an FHA loan. It protects the lender's investment, which is your house itself, from physical damage.

What does a standard homeowner's insurance policy usually cover?

A typical homeowner's insurance policy includes coverage for the structure of your house, other structures on your property, your personal belongings inside the house, additional living expenses if you have to move out temporarily due to a covered loss, liability if someone is injured on your property, and minor medical payments for guests injured on your property.

What kinds of events are typically covered by homeowners' insurance?

Homeowner's insurance usually covers events like fire, windstorms, hail, explosions, riots, damage from aircraft or vehicles, smoke, vandalism, theft, falling objects, the weight of snow or ice, and some types of water damage from things like burst pipes.

Are there things that homeowner's insurance typically doesn't cover?

Yes, most homeowners' policies do not cover earthquakes, floods, landslides, sewer backups (though you can often add this coverage), neglect, pests, and damage from war or nuclear events.

FHA Loan Articles

May 14, 2025When you buy a home with an FHA mortgage, you must pay for both mortgage insurance and insurance to protect your property while paying on the loan. There are important nuances to these insurance policies to know before you start. What's the difference between insurance against water damage and flood insurance? That's just one example of the "hidden" expenses of buying your new home to budget for.

May 13, 2025Buying a home with an FHA mortgage means you'll need to know the FHA guidelines about the types of properties you can purchase with an FHA single-family home loan for residential purposes. How well do you understand these rules? Are you truly ready to start house hunting? We examine some key aspects of the process.

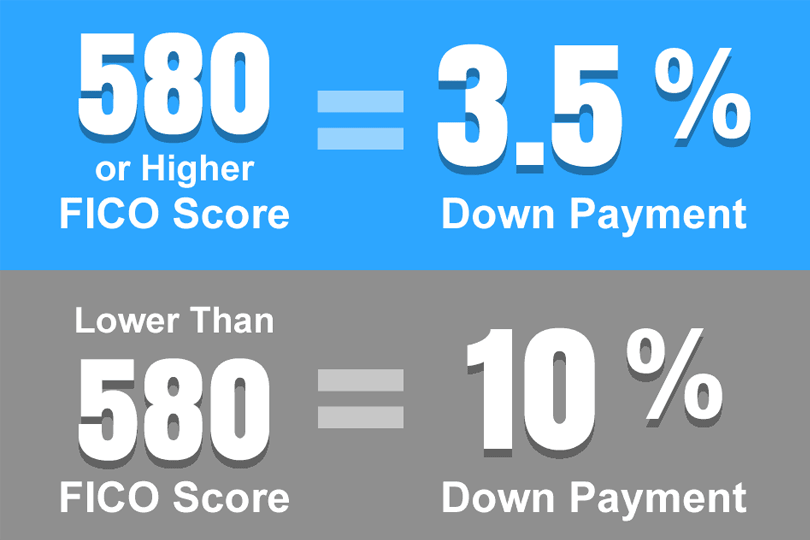

May 12, 2025FHA single-family home loans require a minimum 3.5% down payment for typical transactions. Saving for this requires planning and dedication, but it’s not impossible to save enough to make the down payment. How do people typically budget and save for this? Your financial needs and goals will play a big role in how much you decide to set aside for your new home, but here are some options to think about...

April 30, 2025 In a previous post, we discussed why FHA borrowers should carefully consider whether paying for discount points truly serves their best interests, focusing on factors like short-term homeownership, opportunity cost, FHA mortgage insurance, and the prevailing interest rate environment. Discount points are an option for borrowers willing to pay a fee to lower the interest rate by a set amount. This is not right for all borrowers, and you don't want to pay for points you won't benefit from during the loan term.

April 29, 2025Are you considering buying a home with an FHA loan? You'll likely talk to your participating lender about FHA loan "discount points" – fees you pay upfront for a lower interest rate on your mortgage. The idea behind discount points is a straightforward exchange: you spend money today to reduce your interest rate. Typically, one point equals one percent of your total FHA loan. In return, your interest rate might decrease by an amount you and the lender agree upon.