Fixing Your Credit Score

January 10, 2023

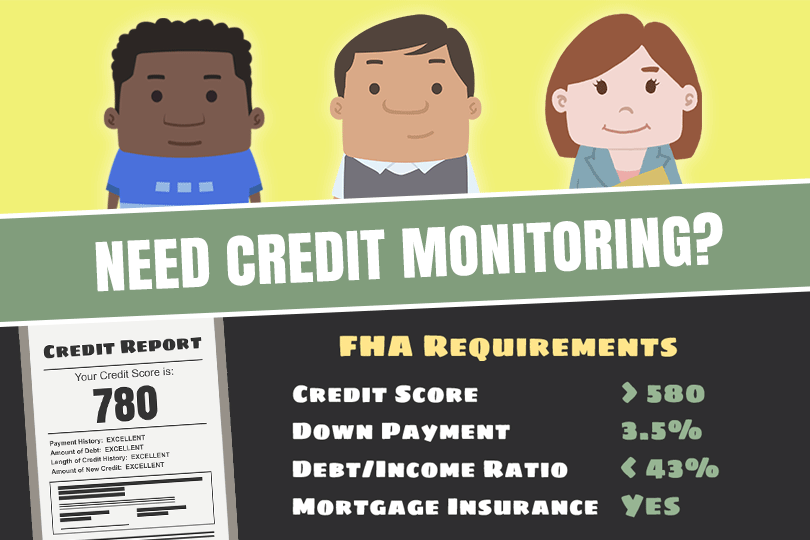

To start improving your credit score, it helps to know what goes into making it. The factors that affect your score are:

- Timely payments: 35%

- Overall debt: 30%

- Length of credit: 15%

- New credit applications: 10%

- Types of credit: 10%

Know Your Score

You need to know what your score is if you want to get started on improving it for a home loan. According to the Fair Credit Reporting Act, individuals have the right to their own credit report, which is available from a credit bureau. You can request your report from these bureaus, the top three of which are Equifax, TransUnion, and Experian. Once you have your report, you can review it and dispute any discrepancies. The bureaus are responsible for investigating any disputes within 30 days.

Don’t Let Your Balance Go Past-Due

The most important factor that makes up your credit score is your payment history. 35% of your credit report depends on whether or not you make payments on time. The later you are on those payments, the worse it is for your credit report. Always try to pay off your credit balances in full. Not only does this keep you from incurring large interest payments, but having a “paid in full” remark on your credit report looks good to lenders considering you for a loan.

Building a Credit History from Scratch

Many first-time homebuyers run into the problem of not having a sufficient credit history. This can affect the 15% of your score that depends on age of credit. Establishing credit history can start with signing up for a credit card and using it to pay for everyday items. It also helps to set up utility payments through your credit card online. Just remember to pay off the balance on time!

Be Proactive About Opening New Lines of Credit

When applying for a loan or credit card, your bank or lender performs a “hard inquiry.” This is a review of your credit that in turn affects your score. If you submit multiple credit applications in a short timeframe, it shows up as a red flag for lenders. They might assume that you aren’t handling your finances well enough if you need multiple lines of credit open at once. It’s important that you don’t submit credit applications close to the time that you apply for a home loan.

Remember that your credit score represents your creditworthiness. Based on this number, a lender determines whether you are a high-risk borrower and if it’s a smart idea to loan you a huge amount of money. It also determines the interest rate you’ll receive from the lender, so it is worth your time to work on increasing your score.

------------------------------

RELATED VIDEOS:

Learn How to Meet FHA Requirements

A Few Tips About Your Fixed Rate Mortgage

Your Proof of Ownership Is the Property Title

FHA Loan Articles

May 14, 2025When you buy a home with an FHA mortgage, you must pay for both mortgage insurance and insurance to protect your property while paying on the loan. There are important nuances to these insurance policies to know before you start. What's the difference between insurance against water damage and flood insurance? That's just one example of the "hidden" expenses of buying your new home to budget for.

May 13, 2025Buying a home with an FHA mortgage means you'll need to know the FHA guidelines about the types of properties you can purchase with an FHA single-family home loan for residential purposes. How well do you understand these rules? Are you truly ready to start house hunting? We examine some key aspects of the process.

May 12, 2025FHA single-family home loans require a minimum 3.5% down payment for typical transactions. Saving for this requires planning and dedication, but it’s not impossible to save enough to make the down payment. How do people typically budget and save for this? Your financial needs and goals will play a big role in how much you decide to set aside for your new home, but here are some options to think about...

April 30, 2025 In a previous post, we discussed why FHA borrowers should carefully consider whether paying for discount points truly serves their best interests, focusing on factors like short-term homeownership, opportunity cost, FHA mortgage insurance, and the prevailing interest rate environment. Discount points are an option for borrowers willing to pay a fee to lower the interest rate by a set amount. This is not right for all borrowers, and you don't want to pay for points you won't benefit from during the loan term.

April 29, 2025Are you considering buying a home with an FHA loan? You'll likely talk to your participating lender about FHA loan "discount points" – fees you pay upfront for a lower interest rate on your mortgage. The idea behind discount points is a straightforward exchange: you spend money today to reduce your interest rate. Typically, one point equals one percent of your total FHA loan. In return, your interest rate might decrease by an amount you and the lender agree upon.