Non-Financial Factors That Affect Home Loan Interest Rates

December 30, 2024

One factor is occupancy type. For FHA loans, this is straightforward because these loans require owner occupancy. Investment properties aren't eligible. While conventional loans may have different rates for primary residences, second homes, and investment properties, this isn't a concern with FHA loans.

Some might not immediately know which loan is best for them, but knowing the occupancy requirement ahead of time can help them make a more informed choice.

Your employment history is another factor. A stable job with consistent income shows lenders you're reliable and can make your mortgage payments. They'll look at how long you've been employed, your income stability, and your industry. Building a strong employment profile can help you get a better interest rate if the lender feels that history shows you are a good credit risk.

The loan term and payoff schedule also play a role. The loan term affects your monthly payments and total interest costs.

The amortization schedule determines how your payments are applied to principal and interest over time. Your lender may offer different interest rates for a 15-year loan compared to a 30-year mortgage, for example.

Standard amortization has early payments mostly going toward interest, while graduated payment mortgages have payments that start lower and increase over time.

Your income projections and financial goals will influence your choice of amortization schedule, and your lender may offer different interest rates for different loan terms and amortization schedules.

Remember, lenders consider various factors when determining your FHA loan interest rate. Understanding these factors can help you make informed decisions and potentially secure a lower rate.

FHA Loan Articles

March 31, 2025Is 2025 the right year for you to consider an FHA streamline refinance? These mortgages are for those who want a lower interest rate, a lower monthly payment, or to move out of an adjustable-rate mortgage and into a fixed-rate loan. We examine some of the critical features of FHA streamline refinances.

March 27, 2025Did you know there are FHA loans that let house hunters buy multi-family properties such as duplexes and triplexes? FHA rules for these transactions is found in HUD 4000.1, including owner-occupancy, require that one unit serve as the borrower’s primary residence. Some house hunters ask why this rule exists. Some believe the rule serves as a lender risk mitigation strategy.

March 25, 2025What does it take to sell a house purchased with an FHA mortgage? Are there special rules, restricrtions, or added considerations? We examine some key questions and their answers to FHA real estate sales issues.

March 24, 2025If you are selling a home, you may need to negotiate with buyers to fund their purchases with an FHA mortgage. What do you, as a seller, need to know about FHA mortgages and how they may differ from conventional loans? We examine some common issues.

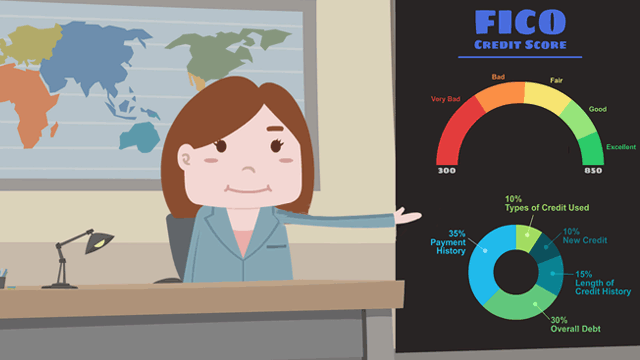

March 24, 2025How much do you really know about how FHA home loan interest rates are set and what factors influence them before your lender makes you an offer? We explore some key points about FHA loan rates, FICO scores, and debt ratios.