Can I Get a No Money Down FHA Loan?

August 14, 2023

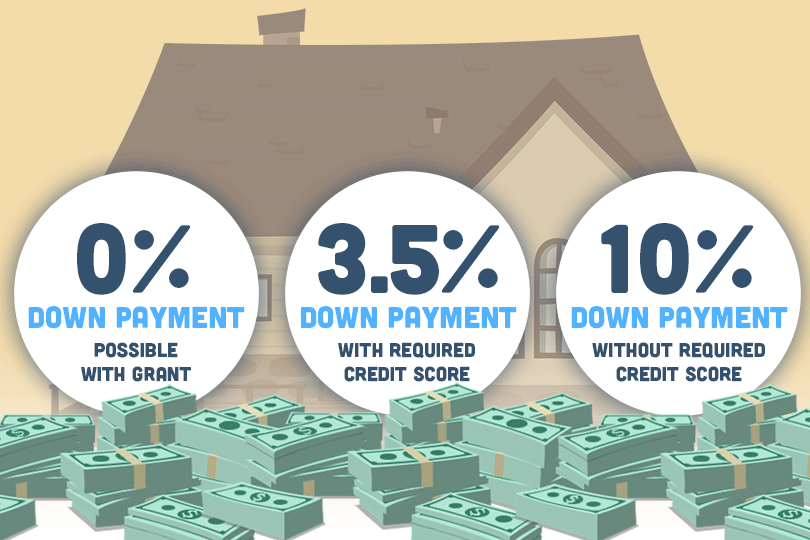

FHA loans typically require a minimum down payment of 3.5% of the purchase price of the home with the right credit score. This means that if you're buying a house for $240,000, you would need to make a down payment of at least $8,400. The down payment can come from your own funds, a gift from a family member, or a down payment assistance program. If your credit score is below the standard requirement set by you lender you may have to increase your down payment to 10% of the loan.

It's important to note that while the down payment requirement for FHA loans is relatively low, you will still need to cover closing costs, which can include fees for appraisals, inspections, title insurance, and more. These costs are separate from the down payment.

Additionally, FHA loans have mortgage insurance premiums (MIP) that borrowers are required to pay, both upfront and as part of their monthly mortgage payments. This insurance helps protect the lender in case the borrower defaults on the loan.

Please keep in mind that loan program guidelines can change over time, so it's a good idea to consult with a mortgage lender or FHA-approved lender for the most up-to-date information on FHA loan options and requirements, especially if you are considering purchasing a home today.

------------------------------

RELATED VIDEOS:

Annual Income Requirements for FHA Loans

Good Credit History Helps Get FHA Loans

Stay Informed About Your Mortgage Closing Costs

FHA Loan Articles

January 15, 2025Buying a condo with an FHA loan is an option some don’t consider initially, but it’s worth adding to your list of potential property types. FHA loans for condo units traditionally require condo projects to be on or added to the FHA-approved list. Still, changes in policy over the years allow borrowers to apply for FHA loans on condo units in projects not on the list on a case-by-case basis.

December 30, 2024When applying for an FHA loan, lenders will consider more than just your credit scores and history. They also look at other factors affecting your risk profile and the interest rate they offer you.

One factor is occupancy type. For FHA loans, this is straightforward because these loans require owner occupancy. Investment properties aren't eligible. While conventional loans may have different rates for primary residences, second homes, and investment properties, this isn't a concern with FHA loans.

December 18, 2024Did holiday spending get the better of you? Are you looking for ways to recover your spending plan as you search for a new home?

The holidays are a whirlwind of festivities, family gatherings, and gift-giving. But amidst the cheer, it's easy to lose track of spending. If you're aiming to buy a home in the near future, those extra expenses can have a bigger impact than you might realize, especially if you're considering an FHA loan.

December 17, 2024The Federal Housing Administration provides mortgage insurance on loans made by FHA-approved lenders, making homeownership more attainable for those who might not qualify for conventional loans.

While financial factors like credit score and debt-to-income ratio are key to loan approval, other non-financial aspects can also cause a denial.

December 11, 2024FHA loans, insured by the Federal Housing Administration, are a popular choice for many homebuyers, especially those who need a lower downpayment or more forgiving credit qualifying requirements. FHA loans are primarily intended for primary residences—homes that borrowers will occupy as their main dwelling.